Global government debt set to soar to record $71 trillion this year: Research

[ad_1]

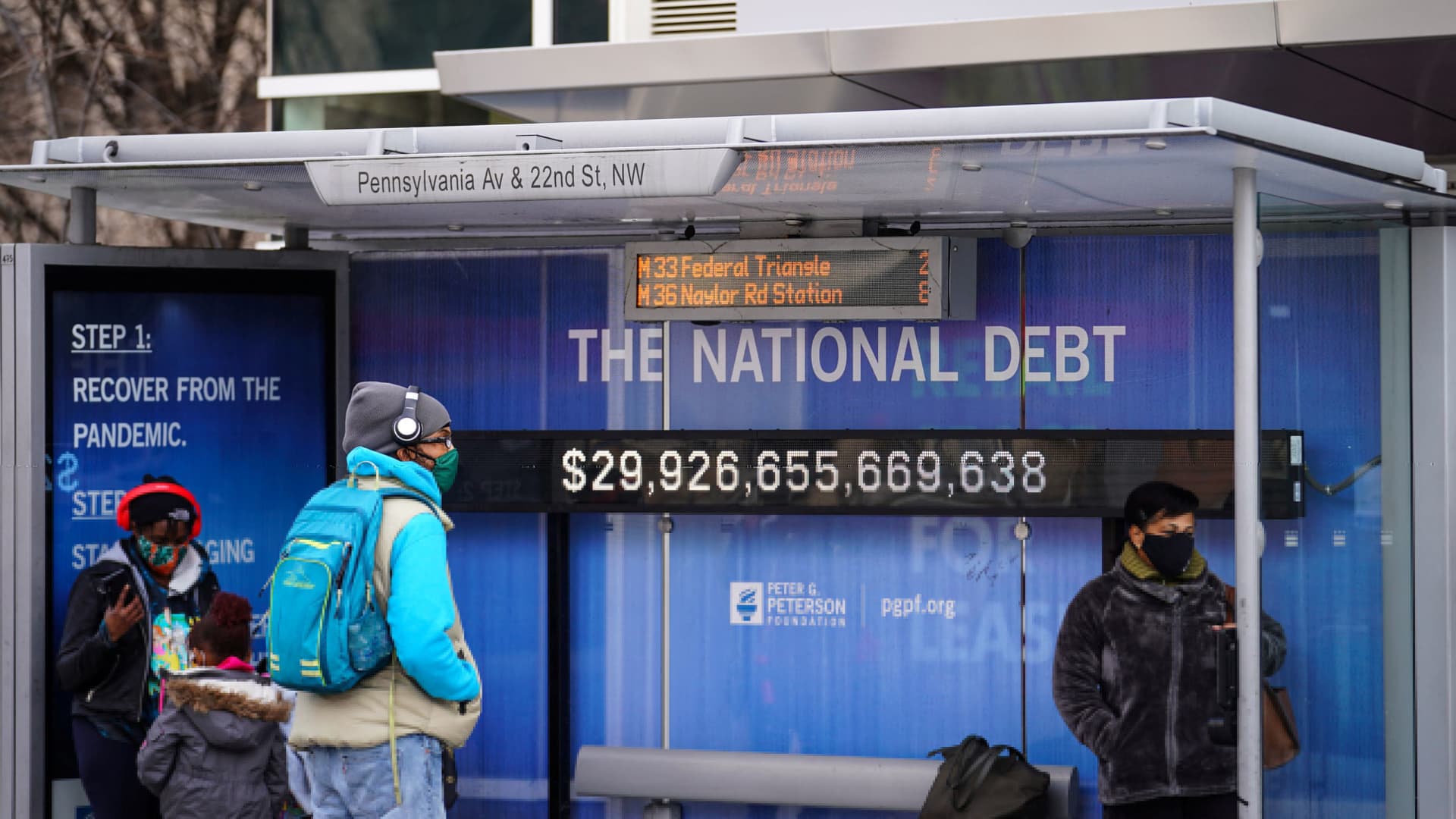

Protective face masks are worn by people who wait in a bus station to see the display of current national debt during the coronavirus pandemic (COVID-19), which hit Washington on January 31, 2022.

Sarah Silbiger | Reuters

LONDON — Global sovereign debt is expected to climb by 9.5% to a record $71.6 trillion in 2022, according to a new report, while fresh borrowing is also broadly set to remain elevated.

Janus Henderson, a British asset manager, projected that global debt would rise 9.5% in its second annual Sovereign Debt Index. This was mainly driven by China, Japan, and the United States, but the majority of countries are expected to borrow more.

The report stated that global government debt rose 7.8% to $65.4 trillion in 2021. All countries assessed experienced an increase in borrowing. However, debt servicing costs fell to a new low of $1.01 billion, a rate effective at just 1.6%.

The debt servicing costs will increase by around 14.5% to $1.16 Trillion on a constant basis in 2022.

The U.K. will experience the greatest impact due to rising interest rates.

“The pandemic has had a huge impact on government borrowing – and the after-effects are set to continue for some time yet. Bethany Payne is Janus Henderson’s portfolio manager for global bond portfolios. She said that the tragedy in Ukraine could also force Western countries to borrow further to pay more defense spending.

Germany has already vowed to ramp up its defense spendingIn a major policy shift after Russia invaded Ukraine, more than 2% was added to GDP. Additionally, 100 billion euros (or 110 billion dollars) were earmarked for a fund that will support the country’s armed services.

New sovereign borrowing is expected to reach $10.4 trillion in 2022, almost a third above the average prior to the Covid-19 pandemic, according to the latest global borrowing report from S&P Global Ratings published on Tuesday.

“We expect borrowing to stay elevated, owing to high debt-rollover needs, as well as fiscal policy normalization challenges posed by the pandemic, high inflation, and polarized social and political landscapes,” said S&P Global Ratings credit analyst Karen Vartapetov.

According to the report, global macroeconomic effects of ongoing conflicts are likely to increase demand for government funding. However, tighter monetary conditions could lead government funding costs to rise.

For sovereigns, which have so far failed to reinvigorate growth or reduce reliance on foreign currencies financing and whose interest rates are high, this creates a problem.

In advanced economies, borrowing costs are expected to rise but likely remain at a level that will allow governments time for budget consolidation, S&P said, offering governments time for budget consolidation and focus on growth stimulating reforms.

Investors have many options

In the early years of the pandemic the theme of convergence in monetary policy was prominent. Central banks cut interest rates at historic lows to support the ailing economies.

Janus Henderson pointed out that divergence has become a major theme as central banks across the U.S. and U.K. look to tighten their policy strings in order to control inflation. China, however, continues to attempt to boost the economy by adopting a more accommodating policy.

Investors in short-dated bonds with less market risk can take advantage of this divergence, Payne suggests, by focusing on two specific locations.

She stated that China and Switzerland are both actively engaged in loosening monetary, while Switzerland has greater protection against inflationary pressures as energy consumes a lower percentage of its inflationary basket. Switzerland’s policy is tied but lagging to the ECB.

Janus Henderson believes that shorter-dated bonds are more attractive than riskier longer-term bonds.

Payne explained that when interest rates and inflation are increasing, fixed income can be dismissed as an asset type, especially since the historical average bond value is relatively high.

However, the value of many asset classes is much higher than that of government bonds and investors weightings are very low so diversification is important.”

She argued that the market has mostly priced higher inflation expectations so today’s bonds have higher yields than those bought a few months back.

[ad_2]